Real estate closing document notarization is the process by which a licensed notary public verifies signer identities, witnesses signatures, and applies an official seal to key real estate transaction documents, making them legally enforceable and eligible for county recording. Without valid notarization, deeds and mortgage documents cannot enter the public record, which means your ownership or lien has no legal standing. Every homebuyer and real estate investor needs to understand what gets notarized, why it matters, and how to prepare so the closing goes through without delays or rejections.

What real estate closing document notarization actually covers

Notarization in a real estate context is the formal act of a commissioned notary public serving as an impartial witness to document signing. The notary confirms the signer's identity, verifies the signature is voluntary, and completes a notarial certificate that becomes part of the legal record. This is distinct from legal advice. A real estate notary guides signers through documents and remains impartial but does not interpret contract terms or advise on legal rights.

The reason notarization is legally required comes down to recording. County recorders will not accept a deed or mortgage without a valid notarial acknowledgment attached. Indiana's recording laws, for example, require proper acknowledgment certificates on deeds and mortgages before they are accepted for filing. The same principle applies across virtually every U.S. state. Without that recorded document, your ownership or lender's lien does not exist in the public record.

Which documents require notarization at closing

Not every page in a closing package needs a notary seal. Mortgage document packages can run 100 to 150 pages, but notarization focuses on the specific documents that must be recorded or that create legal obligations tied to identity verification. Knowing which documents fall into that category helps you prepare and avoids confusion at the signing table.

The core documents that typically require notarization include:

- Warranty deed or quitclaim deed: Transfers ownership from seller to buyer and must be notarized for county recording.

- Mortgage or deed of trust: Creates the lender's lien on the property and requires notarization to be recorded.

- Deed of trust riders: State-specific addenda attached to the mortgage that carry the same recording requirement.

- Affidavits: Statements of fact such as an owner-occupancy affidavit or a title affidavit that require sworn acknowledgment.

- Power of attorney documents: If someone signs on behalf of another party, the POA itself must typically be notarized and recorded.

The table below shows how document types compare in terms of notarization purpose and recording requirement:

| Document type | Notarization purpose | Recording required |

|---|---|---|

| Warranty or quitclaim deed | Transfers title, establishes ownership | Yes |

| Mortgage or deed of trust | Creates lender lien on property | Yes |

| Affidavits | Verifies sworn statements of fact | Sometimes |

| Power of attorney | Authorizes third-party signing | Yes, if used at closing |

| Promissory note | Borrower's repayment promise | No (held by lender) |

Requirements vary by state, lender, and transaction type. Deeds and mortgages generally require acknowledgments notarized for county recording acceptance, but your title company or closing attorney will confirm the exact list for your transaction.

How to prepare for notarization at your real estate closing

Preparation before your signing appointment prevents the most common source of closing delays: missing or incorrect identification and incomplete documents. Follow these steps before you arrive:

- Bring a current government-issued photo ID. A driver's license, state ID, or passport works. Escrow offices commonly require at least one valid photo ID, and some lenders request two forms. Check with your title company in advance.

- Confirm the Closing Disclosure timing. Federal law requires that the Closing Disclosure be received at least 3 business days before consummation. If your lender mails it, add three presumed delivery days. Your notarization appointment cannot happen until that window closes.

- Review your documents before the appointment. Ask your lender or title company to send the package in advance so you can flag questions. Signing under time pressure increases errors.

- Clarify power of attorney requirements early. If you cannot attend in person and plan to use a POA, confirm with the title company that the POA is current, notarized, and acceptable to the lender. Stale or revoked POAs can void the entire transaction.

- Verify the notary's credentials. Ask whether the notary is a certified signing agent through the National Notary Association. Confirm that your lender and title company accept the notary, especially if remote online notarization (RON) is being considered.

Pro Tip: Ask your title company for the full document list at least 48 hours before closing. Experienced signing agents proactively clarify which pages must be notarized and confirm any signer ID exceptions ahead of closing to reduce re-signing delays.

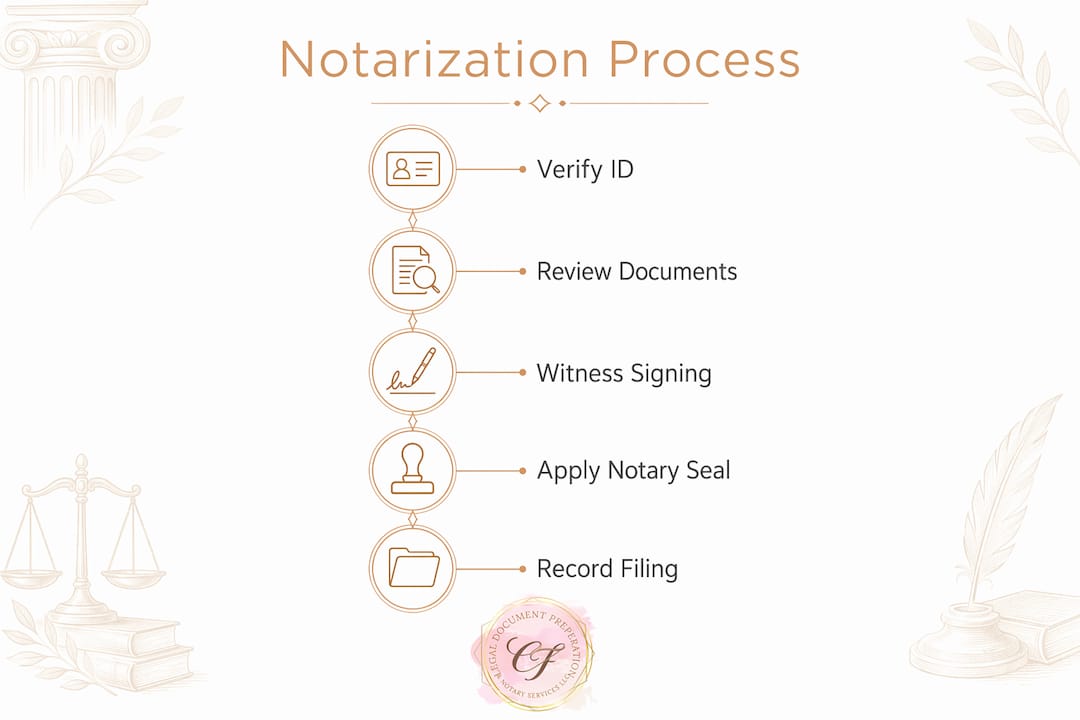

Step-by-step process of notarizing closing documents

Understanding what happens during the actual notarization removes the anxiety most first-time buyers feel at the signing table. Here is the sequence a qualified notary follows:

- Identity verification. The notary examines your government-issued photo ID, confirms the name matches the documents, and may record the ID details in a notary journal.

- Document review and organization. The notary separates the package into pages requiring notarization and pages requiring only signatures. This prevents missed notarizations and unnecessary seal placements.

- Signature witnessing. You sign each document in the notary's presence. The notary confirms you are signing voluntarily and appear to understand what you are signing.

- Notarial certificate completion. The notary fills in the certificate with the correct venue (state and county), the date, your full legal name as it appears on the document, and the appropriate acknowledgment or jurat wording required by state law.

- Seal and signature application. The notary applies the official stamp or embossed seal and signs the certificate. This is the act that makes the document legally complete.

- Document return and recording. Notarized originals go back to the title company or closing attorney, who submits them to the county recorder's office. Recording creates the public record of ownership or lien.

The table below summarizes what happens at each stage and who is responsible:

| Step | Action | Responsible party |

|---|---|---|

| Identity check | Review and log signer ID | Notary |

| Document sorting | Identify notarization-required pages | Notary or signing agent |

| Signature witnessing | Sign documents in notary's presence | Signer |

| Certificate completion | Fill venue, date, names, wording | Notary |

| Seal and signature | Apply stamp, sign certificate | Notary |

| Recording submission | Deliver to county recorder | Title company or attorney |

Common notarization mistakes that cause closing delays

Notarial certificate errors are the primary cause of filing rejections at county recorders. County recorders scrutinize certificates for correct venue, date, names, wording, and seals. A single missing element sends the document back, which can delay your closing by days or weeks.

The most frequent mistakes include:

- Wrong venue on the certificate. The venue must state the county and state where the notarization took place, not where the property is located. These are often different.

- Missing or illegible notary seal. An expired seal, a smudged stamp, or a seal that bleeds off the page causes automatic rejection.

- Acknowledgment versus jurat confusion. An acknowledgment confirms the signer appeared before the notary and acknowledged the signature. A jurat requires the signer to swear an oath. Using the wrong form invalidates the notarization.

- Incorrect or incomplete signer name. The name on the certificate must match the name on the document exactly. Abbreviations or middle name omissions create discrepancies.

- Stale power of attorney documents. A POA that has been revoked or that expired before closing can void the transaction entirely.

Pro Tip: If a notarization error is discovered after closing, a corrective or re-acknowledgment notarization is possible, but it requires the original signer to appear again before a notary. Catching errors before document submission is always faster and cheaper.

How to find the right notary for your real estate closing

The quality of your notary directly affects whether your documents record without issue. Not every commissioned notary has experience with real estate closing packages, and that gap shows up in the form of certificate errors and missed pages.

Use these criteria when selecting a notary:

- Certified signing agent status. The National Notary Association offers a Certified Signing Agent (CSA) designation that requires background screening and training specific to loan document packages. This is the baseline credential to look for.

- Lender and title company acceptance. Confirm that your lender and title company approve the notary before the appointment. Some lenders maintain approved vendor lists.

- In-person, mobile, or RON options. Mobile notaries travel to your location, which is convenient for buyers who cannot reach a title office. Remote Online Notarization enables notarization via live video, but many lenders remain hesitant to accept RON due to costs and inconsistent recording acceptance across jurisdictions.

- Fee transparency. Notary fees for real estate acknowledgments typically range from $5 to $15 per signature, but full closing notary services with travel can run $75 to $200 or more. Ask for a flat fee quote upfront.

- Experience with your document type. Ask the notary directly how many real estate closings they have handled and whether they are familiar with your state's specific certificate wording requirements.

RON adoption is growing but faces real limits. Coordinated approval from the lender, title company, and county recorder is required for an eClosing to work, since notarization quality alone does not guarantee recording acceptance. For most transactions in 2026, an in-person or mobile notary remains the most reliable path.

Key takeaways

Real estate closing document notarization is legally required for deeds and mortgages to be recorded, and certificate errors are the single most common cause of recording rejection and closing delays.

| Point | Details |

|---|---|

| Notarization enables recording | Deeds and mortgages must carry valid notarial acknowledgments to be accepted by county recorders. |

| Know which documents need it | Deeds, mortgages, affidavits, and POA documents are the core notarization-required items at closing. |

| Prepare your ID and timing | Bring a current government-issued photo ID and confirm the 3-business-day Closing Disclosure window before scheduling. |

| Certificate accuracy is critical | Wrong venue, missing seal, or incorrect signer name causes document rejection and delays the entire closing. |

| Vet your notary before closing | Look for a National Notary Association Certified Signing Agent accepted by your lender and title company. |

What I've learned from years of real estate closings

Most closing delays I see are not caused by the documents themselves. They are caused by coordination failures between the lender, title company, and notary. Someone assumes another party confirmed the document list. The notary shows up without knowing the lender requires a specific certificate format. The buyer brings an expired ID. These are preventable problems.

The detail that surprises most buyers is how much the notarial certificate matters compared to the signature itself. You can sign every page perfectly, but if the venue line on the deed acknowledgment lists the wrong county, the recorder sends it back. I have seen closings delayed a full week over a two-word error on a certificate.

My honest advice: do not treat the notary as an afterthought. Hire a certified signing agent with documented real estate experience, confirm acceptance with your title company before the appointment, and ask for the document package in advance. On RON, I think the technology works well in the right circumstances, but the recording acceptance patchwork across Florida counties means in-person or mobile notarization is still the safer default for most buyers in South Florida.

The buyers who close without problems are the ones who ask questions early, not the ones who assume everything is handled.

— Cristina

How Cflegalformhelp supports your real estate closing

Cflegalformhelp provides professional mobile notary and loan signing services across South Florida, with the experience to handle real estate closing packages accurately and on schedule. Cristina Fernandez is a certified legal document preparer who understands exactly which documents require notarization, what certificate wording Florida requires, and how to coordinate with lenders and title companies to prevent rejections.

Whether you are a first-time homebuyer or an investor closing on multiple properties, Cflegalformhelp offers flat-fee, bilingual service in English and Spanish so there are no surprises on closing day. You can also explore the legal document preparation services available for additional closing support. Contact Cflegalformhelp today to confirm your notary appointment and close with confidence.

FAQ

What documents are notarized at a real estate closing?

The deed, mortgage or deed of trust, and any affidavits or power of attorney documents used at closing are the primary notarized items. The promissory note is signed but not typically notarized since it is held by the lender rather than recorded.

Why does real estate closing require a notary?

County recorders require a valid notarial acknowledgment on deeds and mortgages before accepting them for recording. Without that recorded document, ownership and lien rights have no legal standing in the public record.

Can I use remote online notarization for my closing?

RON is legally permitted in Florida and many other states, but acceptance depends on coordinated approval from your lender, title company, and county recorder. Many lenders still prefer in-person or mobile notarization due to inconsistent recording acceptance across jurisdictions.

What ID do I need for closing notarization?

Bring at least one current government-issued photo ID such as a driver's license, state ID, or passport. Some lenders and escrow offices request two forms of identification, so confirm the requirement with your title company before the appointment.

How much does a notary cost for a real estate closing?

Per-signature notary fees typically range from $5 to $15, but a full closing package with travel can cost $75 to $200 or more depending on the notary's services and distance. Always request a flat-fee quote before booking.